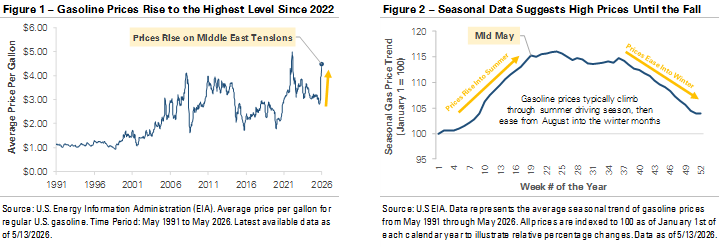

The national average price of a gallon of gasoline has climbed above $4.50, up nearly 50% since the start of the U.S.-Iran conflict in late February. The cause is a global oil supply disruption. Approximately 20% of the world's oil moves through the Strait of Hormuz, a shipping route in the Middle East, and traffic remains significantly below pre-conflict levels. Crude prices have risen as oil supply shrinks, and the price at the pump has followed. The pressure extends beyond the gas pump, with diesel costs feeding into the price of goods moved by truck. The cost increase is starting to work its way into household budgets as inflation pressures build.

Headlines like these tend to generate predictions about where prices go next. Predictions are interesting but rarely actionable. The more useful response is to turn the moment into a short list of questions worth answering. Three are worth discussing now.

A household with two cars is paying roughly $1,200 to $1,800 more per year on fuel than it was earlier this year. The increase is absorbed somewhere, and in most households, it lands in one of two places: the amount being saved each month, or the amount being withdrawn from the investment portfolio. Neither is an incorrect answer, but both are worth being intentional about rather than letting them adjust by default.

The practical question is whether the current absorption is the right one or whether a modest adjustment, such as deferring a purchase or temporarily reducing savings, makes more sense. In most cases, the financial plan accommodates the change without revision. The value is in making the choice deliberately.

For retired households, the question is narrower: is this year's spending tracking the plan, or running ahead of it? A temporary period of elevated fuel and grocery costs usually falls inside the margin a retirement plan is built with, but that's worth confirming rather than assuming.

The check is straightforward: compare actual spending over the past several months against what the plan assumed for the year and look at whether the gap is closing on its own as prices stabilize or widening as higher costs work into more categories. Surfacing the answer early is what makes any response, if one is needed, a small one rather than a large one.

Usually not. The inflation assumption inside a financial plan is a long-run average rather than a forecast of any single year. A stretch of 4% inflation, even one that lasts several quarters, doesn’t meaningfully change a long-run average measured over decades. The plan is designed to absorb this kind of variation without needing to be rewritten.

For clients approaching retirement, the relevant check is whether the savings target they are working toward still matches the life they are planning for. For clients earlier in the saving years, it is a reminder that the cost of the future is not a fixed number, which is why the plan is reviewed and updated over time rather than set once.

These questions are part of the regular planning review cycle, and an environment like this one is a normal input into the work as it happens. The price at the pump is a useful reminder that the cost of living isn't a fixed number, but it's a small input into a plan built around a much longer time horizon.

The plan operates on a longer time horizon than any single price moves, which is the reason it can absorb a moment like this one without needing to react to it.

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.