Back-to-back ceasefires, first between the U.S. and Iran on April 7 and then between Israel and Lebanon on April 16, changed the market's outlook. The agreements removed the worst-case scenario, and the reversal was immediate across markets. The S&P 500 erased all its March losses and went on to set a new all-time high by month-end. The Dow surged over 1,300 points the day the U.S.-Iran ceasefire took effect, its best day in a year. The Nasdaq Index gained nearly +16% during the month, driven by a historic semiconductor rally, and the Russell 2000 small-cap index gained +9.8% and set its own record. The recovery also reached beyond stocks. Credit spreads, which reflect how concerned the bond market is about corporate borrowers, reversed three months of widening in four weeks, and market uncertainty, as measured by the VIX Index, fell to pre-conflict levels.

The relief was broad and fast, but the underlying situation remains unsettled. The Strait of Hormuz, which carries roughly 20% of global oil supply, remains effectively closed, with only a few tankers crossing daily compared to hundreds before the conflict. Oil prices fell sharply on the ceasefire announcements, including the largest single-day decline since 2020, but have since risen back above $100 per barrel. Gasoline remained above $4 a gallon throughout April, and consumer confidence fell to its lowest reading in the University of Michigan survey's 70-year history. The ceasefires reduced fears of further near-term escalation, and investors moved quickly to price that in. However, the oil supply disruption that’s become a part of the conflict has not been resolved.

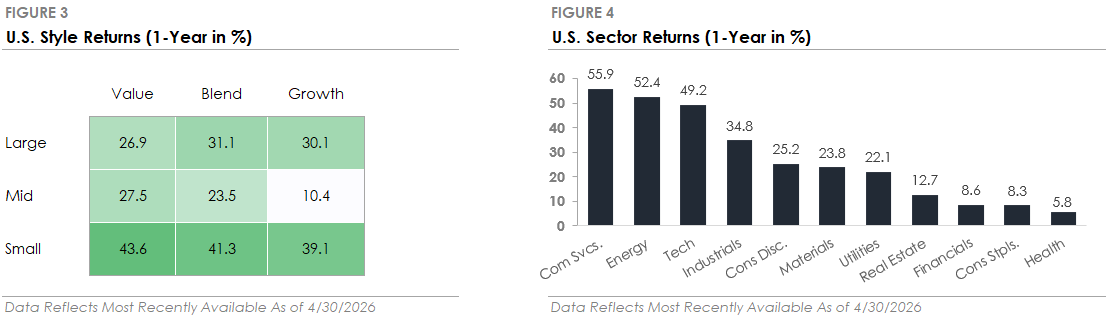

The technology sector gained nearly +18% in April, but the gap between its strongest and weakest corners was wide. The divergence is being driven by artificial intelligence, which is simultaneously fueling demand in one part of the sector and raising fundamental questions about another. AI requires massive upfront investment to build and operate, including computer chips, data centers, power generation, and networking equipment. The companies that build the infrastructure are seeing a surge in demand as the physical backbone behind AI is constructed. At the same time, AI is advancing to the point where it can perform tasks that traditionally require human users interacting with software. AI agents, automated systems that can handle workflows like customer service, data entry, and internal reporting, are raising questions about the future of enterprise software.

The divergence could be seen in markets during April. Semiconductor stocks, which sell computer chips, rose more than +40% over 17 consecutive trading days, the longest uninterrupted winning streak for the group dating back to the early 1990s. Semiconductor funds absorbed $5.5 billion in new investment during the month, and earnings results from major chipmakers confirmed that infrastructure spending is translating into revenue growth. Enterprise software moved in the opposite direction. Several of the largest names in the industry have declined more than -30% this year, and the selling has even hit companies that beat earnings estimates and raised their forward guidance. The divergence comes as the market works through which business models AI will enhance and which it will disrupt. It's a question likely to define not only the technology sector but also the broader market for some time.

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.