Monthly Market Summary

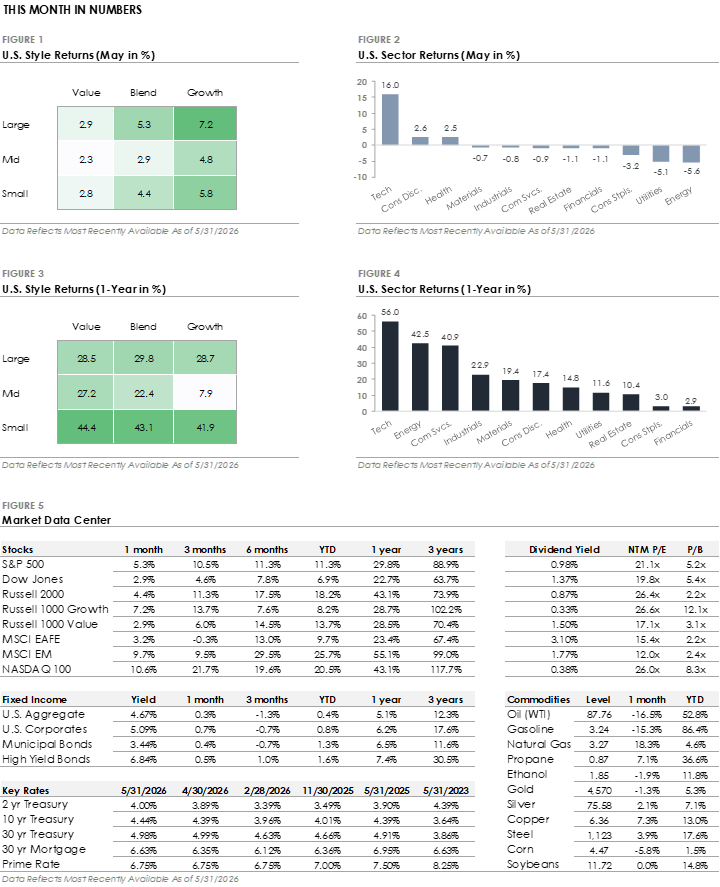

• The S&P 500 Index gained +5.3% in May and set multiple new all-time highs. Technology led all S&P 500 sectors with a +16.0% return, followed by Consumer Discretionary (+2.6%) and Health Care (+2.5%). However, eight of eleven sectors traded lower, led by Energy (-5.6%), Utilities (-5.1%), and Consumer Staples (-3.2%).

• Bonds traded higher despite a mid-month surge in Treasury yields. The U.S. Bond Aggregate returned +0.3% but underperformed corporate bonds as credit spreads tightened. Investment-grade and high-yield corporates returned +0.7% and +0.5%, respectively, with both outperforming the broader Bond Aggregate.

• International stock traded higher in May but were mixed. Emerging markets gained +9.7% and outperformed the S&P 500, while developed markets' +3.2% return lagged both U.S stocks and emerging markets.

Stocks Set New Highs as Geopolitical Tensions Ease

May was a strong month for equities, with most major indexes setting fresh all-time highs. The S&P 500 and tech-heavy Nasdaq 100 set new highs each week, with the Dow Jones and Russell 2000 also setting new highs throughout the month. Even the equal-weight S&P 500, which gives each company the same weight regardless of market cap, set a new high. While the equal-weighted index's move signals broadening participation, leadership was narrow within the index. The technology sector gained +16% and was the only sector to outperform the S&P 500 Index. Eight of eleven S&P 500 sectors traded lower, and ten of eleven sectors underperformed the index. The concentration showed up in factor indexes as well, with large-cap growth returning +7.2% versus +2.9% for large-cap value. The performance gap highlights a notable trend this year: AI and tech stocks continue to outperform more traditional, cyclical companies.

Bonds also traded higher, with the U.S. Aggregate Bond Index returning +0.3% and corporate bonds outperforming as credit spreads tightened further. The bond market’s gains came despite a surge in interest rates mid-month. The 30-year Treasury yield spiked above 5%, reaching levels last seen in 2007, and the 10-year Treasury set a new 52-week high. The trigger was back-to-back hot inflation reports for consumer and producer prices, with the Middle East conflict and elevated oil prices creating broader price pressures. Following the inflation reports, the market now places a greater than 50% probability of a Fed rate hike at the December 2026 meeting, a significant shift from earlier in the year when the market assumed a rate-cutting path. With Treasury yields at multi-decade highs and oil prices leading to inflation concerns, the bond market is shifting toward interest rates remaining higher for longer.

This Year’s Two Defining Themes: Geopolitics & Artificial Intelligence

Two themes have defined markets this year. The first is geopolitics. Trade and tariff uncertainty earlier in the year has given way to military conflict in the Middle East, which has created an oil supply disruption. The Strait of Hormuz, which carries roughly 20% of global oil supply, has been effectively closed since the conflict began in late February, causing global oil inventories to shrink. Oil prices remain elevated after briefly hitting four-year highs earlier this year but have been relatively contained given the extent of the oil supply disruption. There was partial relief in May as U.S.-Iran negotiations progressed and the market began pricing in a potential reopening of the Strait. West Texas Intermediate crude ended the month below $90 per barrel, down -16.5%. However, the path forward remains uncertain, as a successful deal would take months to restore shipping traffic to pre-conflict levels. What happens next in the Middle East will impact energy prices, the inflation outlook, and the broader financial market.

The second theme is the artificial intelligence buildout. Companies have committed hundreds of billions to build the AI industry's physical backbone, including data centers, computer chips, and power generation. Forecasted 2026 capital spending across the leading tech companies now exceeds $600 billion, with most of the capex directed at AI infrastructure. The spending is driving economic growth and starting to show up in corporate earnings, with AI-linked revenue growth becoming a significant driver of overall S&P 500 profit growth. The investment is also creating drastic changes. Shortages across parts of the technology supply chains are creating bottlenecks, and companies are experiencing rapid growth as they repurpose products and services for the age of AI. The pace of spending and technological change explains much of the performance gap between the tech sector and more traditional areas of the stock market.

Important Disclosures

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.