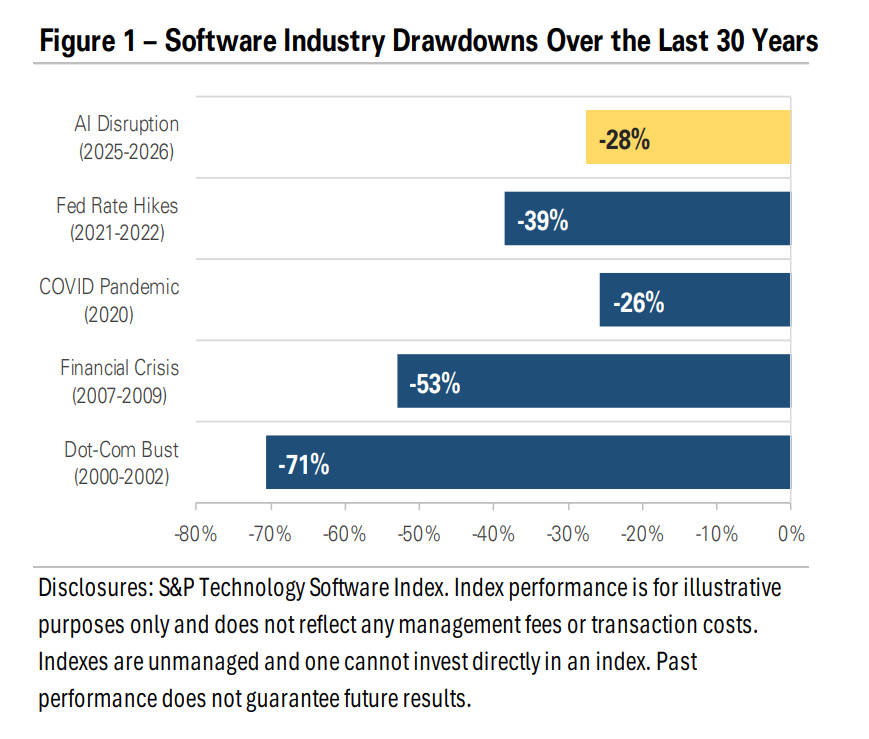

The software industry has declined nearly -30% from its peak last October, one of the largest non-recessionary drawdowns in over 30 years. Figure 1 puts the decline in historical context alongside the other major software selloffs. The two largest drawdowns before the current one, the dot-com bust and the 2008 financial crisis, both occurred during recessions, when corporate earnings were declining and businesses were cutting spending. The 2022 selloff, driven by the Federal Reserve’s aggressive rate-hiking cycle, was the first major non-recessionary decline and saw software stocks fall nearly -40%. The current drawdown, at nearly -30%, surpasses the COVID pandemic, but it’s driven by a fundamentally different catalyst: artificial intelligence.

The sell-off accelerated in January and February after a series of artificial intelligence (AI) product launches showed that general-purpose AI tools could perform tasks previously handled by specialized software at a lower cost. The market’s reaction was swift and sequential. Software stocks fell first, but concerns quickly spread to other industries, including financial data providers, commercial real estate services, and logistics companies. The sell-off reflected a shift in how investors view AI. For the past two years, AI has been seen as a productivity tool that would help existing companies do more with less. The January and February product launches crossed a threshold: investors started pricing AI as a potential replacement for entire categories of professional services, not just a tool to make companies more efficient.

By late February, the narrative around AI disruption began to cool and markets started to stabilize. Wall Street analysts pushed back on the worst-case scenarios, and the conversation shifted from AI would replace entire industries to a more focused debate about which industries are genuinely vulnerable and which will find ways to adapt and develop competitive advantages. Several of the hardest-hit stocks rebounded, and while the software industry partially recovered, it remains down more than -25%. The broader question of how AI will reshape professional services and the enterprise software industry is far from resolved, and its effects may continue to surface across the market as AI tools evolve.

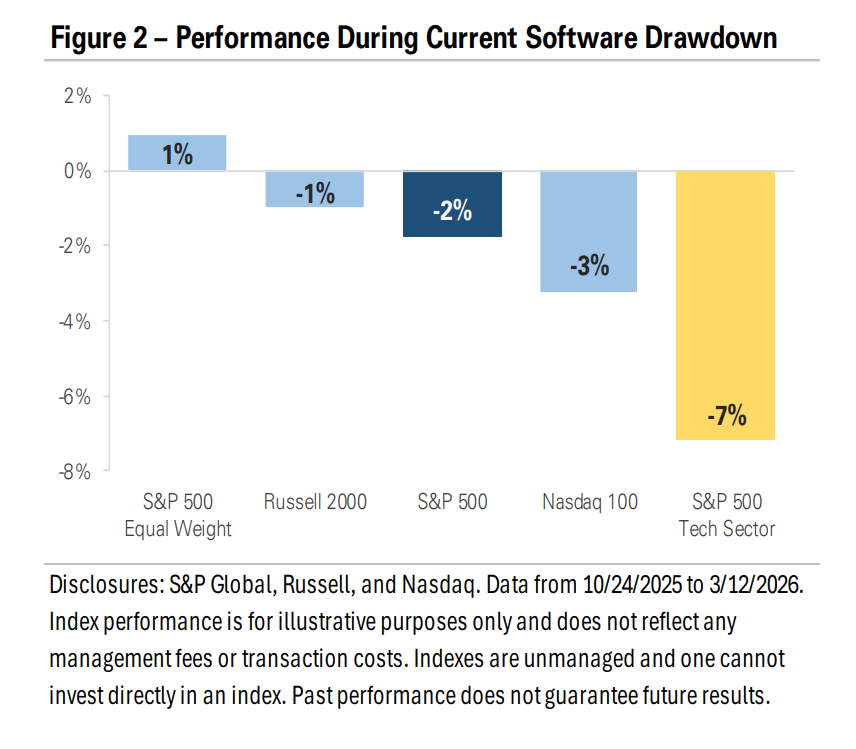

The software industry’s sell-off is a reminder that even well-established businesses can experience rapid repricing when the market’s assumptions about future earnings change. However, Figure 2 shows the direct impact has been limited for diversified investors. International stocks and the average S&P 500 stock have both produced gains, while small-cap stocks, the broader S&P 500, and the Nasdaq 100 are each down low single digits. The takeaway: portfolio diversification across sectors and asset classes remains an effective way to manage the uncertainty that comes with rapidly changing environments and market volatility.

Important Disclosures

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.